Updated: June 5, 2012 (Initial publication: June 4, 2012)

Releases : I. Isolated Articles

I-1-44: Time for Sovereignty: Sovereign Wealth Funds and Sovereign Ratings.

Attached documents

The paper considers the interactions among time, finance, and sovereign power. It is argued that an inverse relationship between State sovereignty and time acceleration can be verified, which is examined vis-à-vis different types of States, Sovereign Wealth Funds and Credit Rating Agencies, and financial intermediaries. The paper examines the challenges imposed to sovereignty by the activities performed by Sovereign Wealth Funds, and the semi-public functions carried out by Credit Rating Agencies. The possibilities of a “curvature” of the constitutional space, and of a “slow acceleration” of sovereign power are further discussed.

Summary: 1. Time, sovereignty and finance.

– 2. The rise of sovereign wealth funds. – 3. Rating the sovereign? –

4. Tentative conclusions. [1]

1. Time, sovereignty and finance.

The paper examines the notion of sovereignty from the viewpoint of the relationship among finance, time and sovereign power. Hence, we consider the way in which sovereignty shapes the constitutional system, and the meaning that this notion appears to have assumed following to evolutions in the political and economic spheres.

The relationship between finance and sovereign power is certainly not new. It may be sufficient to recall the role played by Italian bankers from the XIIth century onwards in lending to sovereigns (especially those of France, England and Spain), in exchange for the control of goods of primary importance (which could be produced or traded only under royal license)[2]. Being financed often entailed for the sovereign the acceptance of “conditions”, potentially resulting in a “privatization” of some governmental functions (e.g. a direct pledge on the tax revenues of the State). Therefore, to different extents the public power sometimes appeared to have given up sovereignty over parts of the economy due to finance itself.

What’s new is that in order to examine such relationship we make use of another instrument: time. We argue, in fact, that time may be a valid pivot for the understanding of the tension in place between sovereignty and financial power.

In order to do this, we assume that the relationship between time and sovereign power may be summarized by a model under which

k=(temporal guarantees + x0 )/power

where the constitutional rate equals the sum of temporal, structural and functional guarantees plus the protection of rights, divided per the amount power. In other words, our starting idea is that an inverse proportion may be verified between the control of time by mean of the power, and the protection of those who are subject to that power[3].

This inverse proportion has to be borne in mind while considering the temporal profiles of Constitutions, to which insufficient attention is often paid. Constitutions express a relation with the past since they are frequently created as a result of revolutions, or as a response to previous setbacks in the protection of liberties and rights. Positively, they are also linked with old national traditions and memories. As for the present, they bear a positive legal weight, due either to the direct applicability of constitutional norms, or to standstill clauses (under which no deterioration in the interpretation can occur before legislative implementation of the Constitution takes place). Finally, Constitutions are legal documents approved to last over time, thus comprising norms gifted with a teleological character, and committed towards future generations, thus bearing s significant relation with the future[4].

Coming closer to the relationship between sovereign power and finance, the starting point should be the observation that the predominant link of finance with the time dimension has resulted in the past decades in an acceleration imposed to contemporary economy. In turn, this determined an acceleration on contemporary public institutions, along with phenomena of redefinition of the geopolitical equilibrium at the global scale.

From a dynamic point of view, sovereignty should therefore be examined in the light of the acceleration of institutional times. At the systemic level, slowness is generally associated with a more thoughtful reflection over public interest and democratic control, whereas speed is associated with poor dialogue and thin consideration of different interests. From a functional viewpoint, this is reflected in forms of “normative consumerism”, due to which legal norms lose their vocation to eternity and stability and become “consumption goods”. An increase in the legal instruments used for urgent purposes may be witnessed in a number of countries – being there a state of crisis or not – as another expression of a crisis of the law. This, in turn, seems to witness a crisis of the “elective affinities” between capitalism and the rule of law, that becomes even more clear in relation to the ongoing changes in the role of western Parliaments, often reported to be unable to outline true political projects. Along with the increasing reduction of the time of financial transactions, the legislator assumes the features of the “motorized legislator” feared by Schmitt, who highlighted the danger of the necessity to take decisions in increasingly short time, looking for efficiency, at the detriment of democratic dialogue[5].

To complete the outline of the framework presented, it is necessary to combine the elements above with the effects produced – starting from the last decades – by the fading of national borders and the dematerialization of capital. The lack of physical boundaries between capital and territory, along with the virtual character of wealth, result in serious difficulties in defining the idea of the wealth of nations, in relation to which sovereign power may be exercised (as postulated by the principle, increasingly in crisis, that cujus regio, ejus oeconomia[6]).

Given the equation above, the strong relation between finance and time reduces the room for guarantees, to the advantage of power. But the clearing of national borders and the rise of de-materialized finance makes it difficult to read the relationship among sovereign power, time and finance in the light of the traditional meaning of sovereignty as ius excludendi alios, the right to exclude the others.

As a consequence, it is of utmost importance to figure out the ways in which sovereignty is being challenged by external factors. In fact, as far as the meaning of sovereignty as autonomy and independence is concerned, this is conditional to understand the extent to which it is still worth talking about sovereignty as a cornerstone of western legal tradition. We argue that to this purpose it is helpful to take into account the inverse relationship between State sovereignty and time acceleration, in relation to both public and private subjects performing public or semi-public functions.

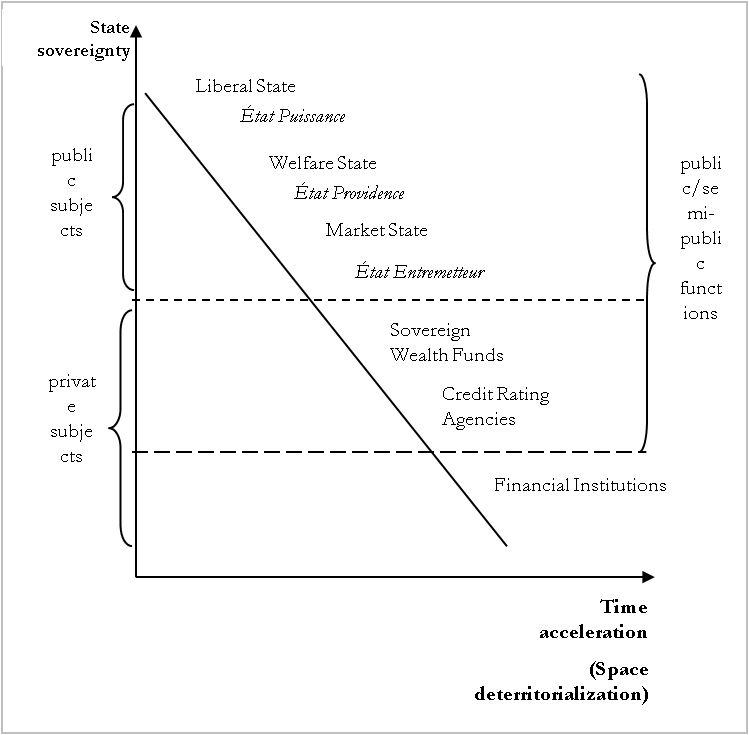

Figure 1. State sovereignty and time acceleration. |

{kind=link}

Figure 1 aims at illustrating graphically the relationship between State sovereignty and time, when a diverse set of public and private subjects is concerned. An inverse relationship may be verified between the two parameters, so that the lower the State sovereignty involved (in terms of authoritative decisions bearing legal and political force), the higher the time acceleration (in term of possibility that actions of these subjects change over time). A similar relationship may also be observed relatively to space de-territorialization, i.e. the possibility that these actions bear little link with national boundaries.

The relationship observed is not a static one, but may change in time due to economic, social and political factors. As a consequence, all the subjects may move upward or downward in the slope as they modify the characteristics of their action, due to endogenous or exogenous factors.

First, let’s consider some of the different types of State that have been identified by the legal doctrine, with regard to the relationship between State and the market. In the classic conception of the Liberal State, administrative and economic functions were performed well separated from the market[7]. The guarantee of civil liberties was an expression of the power (puissance) of the State, that only lately has become to some extent constrained by economic resources, which have been proved to be functional even to the protection of civil liberties[8]. With the development of the Welfare State, sovereign power was entrusted with the performance of activities that brought increasing overlaps with the market, being functional to the satisfaction of new economic and social rights. This kind of State is more dependent on economic contingencies, that may bring in time changes to the activities performed, also due to the economic resources available (as it has been put forward by those underlining the possibility of a fiscal crisis of the State[9]). The third kind of State labeled as Market State[10] identifies a State intervening in the economy in different forms. There can be a direct intervention in economic activities due to the existence of market failures; the performance of specific regulatory tasks; the rescue of economic actors[11]; and most of all the mediation among economic actors[12]. This kind of State – increasingly disaggregated[13] – is highly influenced in time by economic constraints and events, that may significantly shape its actions. Moreover, from a regulatory point of view, it is often subject to changing pressures coming from economic actors, that may give birth to phenomena of regulatory capture[14], occurring in particular when the preferences of the regulated subjects are homogeneous, and in contrast with those of consumers, and the regulators suffer from strong informative asymmetries[15].

The evolution of western States in the last centuries shows a slow movement downward in the slope, with increasing challenges to State sovereignty as traditionally intended, accompanied by a general increase in the role of economic events and in the speed of response by public powers. This tendency may well be witnessed by the attempt of sovereign States to reverse it, e.g. by imposing constitutional constraints to public debt, and therefore to the possibility of the State to borrow in time of crisis[16].

The complex relationship between State sovereignty and time acceleration may be further clarified by the characteristics of some private actors that – either in relation to their origin or their activity – retains significant links with State sovereignty. To this purpose, we consider Sovereign Wealth Funds (SWFs) and Credit Rating Agencies (CRAs) as two subjects at the cutting-edge of contemporary legal and political transformation, to which insufficient attention has been paid until now from a public law viewpoint. We will concentrate later in the paper on their characteristics, being sufficient for now to underline common elements like the fact that they seem to blur the public/private border, and to give additional value to the mobility of production factors, thus fostering competition among sovereign States. SWFs and CRAs therefore occupy an intermediate position between the different kind of States and private actors, due to the performance of semi-public functions, and to a time acceleration incorporated in their activities that is higher than the former, while lower than the latter.

The lowest bottom of the slope is represented by financial institutions, those private actors operating globally within the timeframe of the globalized economy and of instantaneous finance, that may easily become a “dis-insituent time” when compared to the time and rules of public powers and Constitutions[17]. This phenomenon has got even sharper due to the acceleration imposed to capitalism in the last decades, often referred to as “turbo-capitalism”[18], that made financial institutions work at a rhythm even incompatible with public oversight and regulation. This point is well illustrated by a practice that has spread in capital markets worldwide with the name of High-Frequency Trading (HFT). This is a special type of automated trading that enables financial institutions to make transactions at an incredibly high speed. While automatically and instantaneously executing orders in the market, institutions equipped with the appropriate technologies are able to collect information on investments in fractions of seconds (the so called “thirty-milliseconds advantage”), and change investment strategies or make investment decisions in order to maximize profits. HFT is nowadays performed by almost every trading desk of the major investment banks acting as market-makers, thus making the price and providing liquidity for the whole market. HTF interests nowadays approximately 70% of US stock market daily transactions[19].

It is not of our interest to discuss whether HTF may prove useful for markets (because it provides them with more liquidity, helping aligning prices in different markets), or should be prohibited (as a mean of making profits at the expenses of “slow-moving” financial institutions, increasing volatility in the markets, bringing low-quality liquidity and false market signals). What is worth noting is that due to its extremely high speed this practice does not allow any regulatory activity, preventing regulators from carrying out any effective surveillance on the markets. From a regulatory viewpoint, the US Justice Department and SEC recently opened a joint investigation into HFT practices, whereas in Europe the issue is likely to be addressed within the regulatory reform of financial markets under MiFID[20].

2. The rise of sovereign wealth funds.

Sovereign wealth funds (SWFs) – as publicly originated funds operating at the global level with significant economic capacity – challenge the traditional interpretation of the notion of sovereignty for a number of reasons. The phenomenon of SWFs has been quite extensively analyzed during the economic and financial crisis, but the appropriate attention still has to be paid to the deeper legal implications of their operations.

SWFs are a direct effect of economic and financial global imbalances, leading to the accumulation of foreign-currency-denominated reserves. Even though the phenomenon is not completely new, it has nevertheless assumed new characteristics due to the volume and rhythm of the accumulation of reserves, their property concentration and geographical distribution[21]. Moreover, an evolution in the management of reserves has been verified, from highly liquid and low risk/low return investments, to other instruments such as corporate bonds, blue chips and derivatives. The reason for this shift may be found in the will to pursue long-term objectives, like the stabilization of public revenues and the intergenerational transfer of wealth[22]; these are the reasons, in fact, for the establishment of SWFs.

A SWF may be generally defined as a legal entity (more or less independent) controlled by the government, the central bank or another public institution, which is fed by foreign currency official reserves (or royalties on national export). Its institutional task is to manage domestic or third-country investments, with the aim of ensuring the intergenerational transfer of resources, the stabilization of public revenues and the funding of welfare spending. As it has been put forward, SWFs belong to the broader and non-homogeneous category of foreign government controlled investors, which also include similar public entities like State-owned enterprises[23].

From a legal point of view, SWFs represent an attempt to blur the distinction between the public-private legal categories. In the slope illustrated in Figure 1, SWFs assume some characteristics of public institutions, like the reliability and the orientation to the long-term, while at the same time trying not to be associated with political interests and goals of the home State (in any case, a lot of time seems to have elapsed since the British East India Company prevented King James I and King Charles I from entering in the corporation stock due to the fact that they were sovereigns[24]).

Many commentators stress the fact that SWFs contribute to both global growth and financial stability, in a number of ways. They helps maintaining an open flow of resources for long-term investments, provide liquidity for the stabilization of fiscal deficits, and contribute in supporting financial institutions by recapitalizing financial institutions hit by the crisis[25].

Nevertheless, issues such as the decision of the admission of SWFs investments, the enactment of sensible laws and regulations, the state of diplomatic relations, show a change in the characteristics of sovereign power held by the host State. While being less and less independent and isolated from other States, host States are now also exposed to the empasse of taking advantage of investments ensured by SWFs, and the possibility that this might bring the country under indirect influence of home States.

This possibility rests upon two main reasons. The first is that the high economic capacity of SWFs may be directed towards key national networks, resources and facilities. Host States, while interested in promoting foreign direct investments (that to some extents are necessary to enhance the national economy and foster the Welfare State) fear that SWFs investments may sensibly influence the country’s economy. The second reason is that investment decisions may be driven by political reasons, rather than economic ones. This is why SWFs have been blamed of “shaking the logic of capitalism”[26], due to the fact that investments may be driven by reasons other than the maximization of profits. In particular, decisions may also consider the interest of the home State in the access to energetic resources, telecommunications, strategic markets and logistic, an attempt towards technological appropriation, the access to confidential information and knowledge, the influence on host State public opinion.

The reason is fairly clear then, why the greater challenge to State sovereignty seems to come no longer only from private multinationals, but also – and perhaps mostly – by the so called “State capitalism”[27]. By mean of the responses to the financial crisis and the rise of SWFs, it seems to have had the upper hand over free-market capitalism[28].

While the overall legal implications remain unclear, for sure SWFs bring to the extreme consequences the legal issues risen by foreign direct investments. As an answer to that, different regulatory responses have been put into place. While at the soft-law level there has been an attempt to find a multilateral solution (thanks to the efforts of IMF and OECD), the hard law level has been jealously defended by national States, that acted with different instruments and purposes[29].

Regardless of the regulatory answers put in place by host States, there are common issues that from a theoretic point of view concern both home and host States, and specifically relate to the notion of sovereignty. SWFs, in fact, significantly contribute to bring into light some evolution of the notion of sovereignty already in place, while also raising new questions.

The first basic issue relates to the possibility to keep on distinguishing between internal and external sovereignty. The generalized shift from independence to interdependence in the international legal order is made self-evident with the investments of SWFs, that to a certain extent prevent from drawing a clear boundary between the two. Those acts that are expression of national sovereignty (being they the enactment of laws and regulations or the decision to set up and govern a SWF) become inevitably intertwined with the international dimension and the influence upon other sovereign entities. This is also the reason why it becomes increasingly unsatisfactory to distinguish between acts iure imperi (made in the sovereign capacity of States) and acts iure gestionis (made in their private capacity), partly because these two expression have changed their meaning, and seem now to overlap. As a consequence, investments of SWFs seem to bear the characteristics of a “quasi-sovereignty”, i.e. even if they are not entitled to sovereign immunity, they are nevertheless vested with significant public elements. A specific intertwine between the notion of sovereignty and SWFs is also related to the territorial element. In the light of the complex contemporary relationship between territory and the legal space, we may read the investments of SWFs as new forms of “extra-territoriality”, rather than violations of territorial sovereignty. These investments shed light on the possibility that (semi-)public ownership takes place within the territory of another sovereign State. This possibility is still to figure out from a theoretical viewpoint, mainly due to the fact that “sovereign power is […] territorial in character”[30].

In addition to this, SWFs investments put into question the relationship between sovereignty and property. In fact, they seem to push for a “proprietary” idea of sovereignty, intended as the maximization of wealth for redistribution and hegemonic purposes, even beyond the traditional distinction between dominium and imperium. They also seem to challenge the traditional meaning of property as the central institution of capitalistic society. In an increasingly interdependent world, the definition of property as a despotic dominion that may be claimed and exercised in total exclusion of the right of other individuals (as in the 1766 Blackstone Commentaries) seems to lose weight as compared to the idea of access[31]. If goods are decreasingly products, and increasingly contents of possibilities (think for instance to key infrastructures), the right to exclude the others becomes less important than the right not to be excluded from use or enjoyment. While plainly true for the so called “global public goods”, with SWFs this idea gains some importance in relation to national goods as well.

Finally, SWFs seem to call for a review of the notion of monetary sovereignty, challenged by the management of foreign currency reserves by central banks. The traditional meaning of monetary sovereignty, defined as the power to increase or decrease the denomination, quantity and percentage of precious metal in the money[32] has to be nowadays reconciled with an enquiry on the power – for entities entrusted with monetary sovereignty, being either nation States or supra-national entities, like the EU – of effectively govern their currency[33]. Loopholes in the functioning of financial safety nets compelled States (especially developing and emerging countries) to rely on the accumulation of reserves, now feeding the investments of SWFs. This, in turn, increasingly exposes sovereign States and entities to international speculations.

Finally, it is of great importance to underline how SWFs relate to the tension between time and sovereign power. The role they had during in the economic and financial crisis – acting as stabilizers, and sometimes as de facto lender of last resort – makes it clear that their time horizon is the long-term one. As a consequence, the capital flows from surplus countries to deficit countries and their re-allocation towards long-term investments put them in an intermediate position between public institutions and other private subjects in Figure 1. This is due to the performance of functions that, even maintaining a private character, share some characteristics with public ones. In particular, in several occasions SWFs acted as “strong hands” for the economy, avoiding the “short sight” that affect financial markets, pushing them towards short-run speculation[34]. It is also due to the reliability of these long-term investors that somebody advocated the need for rules favoring this type of investments. From a regulatory viewpoint, it is of no doubt that appropriate rules relatively to balance-sheet, prudential supervision, fiscal policy and corporate governance[35] would foster the creation of wealth and financial stability. Nevertheless, while it would be relatively easy at the national level, the high reliability of SWFs is likely to be heavily weighted towards the widespread feeling of a danger imposed upon national economies.

3. Rating the sovereign?

Credit Rating Agencies (CRAs), as private agencies giving ratings to a number of economic and financial parameters, have come to perform a semi-public function, in particular as far as public entities are concerned. Their existence is generally associated with the cognitive need for simplification, that of incorporating information[36] about the credit quality of borrowers, including sovereign entities, corporations, financial institutions, and their related debt offerings[37]. In this way, they allow borrowers to reduce information costs, to access the market and attract investments, and to guarantee appropriate levels of liquidity[38].

Country rating, as opposed to sovereign rating, is generally meant to measure any kind of risk related to a country, i.e. to the possibility that a borrower will be able or willing to pay due to natural, political and economic events in the country (normally, the risk of natural and climate disasters, socio-political risk and economic risk). On the other hand, and more interestingly, sovereign rating is the credit risk in direct relation to the national government. Even though a high correlation may be verified between the two, the latter maintains specific characteristics that shed light both on the evolution of the notion of sovereign power and on its relationship with time.

In the credit rating process[39], sovereigns are divided into two broad categories, “investment grade” and “speculative grade”, and are given ratings ranging from AAA (triple A) to SD (selected default) with a number of intermediate measures (AA, A, BBB, BB, B, CC/CCC). The rating quantify the sovereign risk, i.e. the risk of exposure to default associated to elements that are under control of the government, and out of control for individuals or private firms. The risk specifically pertains to the danger that the national government may enact laws aiming at either declaring bankruptcy or restructuring unilaterally debts towards foreign investors, therefore not servicing its debt obligations in full and on time”[40]. As regards sovereigns, CRAs consider both the ability to pay, intended as the absence of economic or monetary constraints, and the willingness to do it, because of the limited legal redress that may be recognized in case a decision is taken not to meet obligations in full.

It is much interesting is to consider the key parameters considered within the methodology profile, i.e. the institutional effectiveness and political risks, the economic structure and growth prospects, the external liquidity and international investment position, the fiscal performance and flexibility, and monetary flexibility[41].

What is also worth noting is that all these parameters affect each and every moment of the life of a State. By lying at the very heart of national sovereignty, they show how key national decisions may be exposed to the judgment of the markets on a continuous basis.

The heavy implications of sovereign credit ratings over the implementation of national policies puts into question the contemporary meaning of the ius excludendi alios, the right to exclude the others, that is generally regarded as the core element of national sovereignty. What right of excluding the others do countries exposed to credit rating processes retain? Moreover, the increasing tendency of public debt to be held by non-resident investors may be driven either by a strong trust in the issuer (i.e. the sovereign) or by geo-politic interests. In any case, the country is exposed to pressures via both sovereign issuer ratings (related to the State, directly affecting the government), and sovereign issue ratings (related to the single emission, directly affecting public deficit and debt).

One argument put forward by CRAs is that sovereign credit ratings tend to be instruments both neutral and consistent with reality. It is certainly true that the relative rank of sovereign ratings has been consistent with historical default experience[42]. But while it is surely possible to show a correlation between sovereign ratings and sovereign defaults in reality, it is much more difficult to test whether sovereign ratings themselves possibly exerted influence upon the country’s performance and subsequent default.

This last observations helps clarifying how delicate the credit rating activity may be, deprived of guarantees and protection others than the judgment of the market. Moreover, CRAs interfere with the sovereignty of States in their quality of private subjects affected by a number of constraints. CRAs suffer from a conflict of interest arising from the fact that they are pushed to over-rate sovereigns in order to have broader room for the rating of other borrowers in the country (sovereign rating generally represents the maximum rating possible for subjects within one given country). What’s more, as profit-oriented firms, they face budgetary constraints, and thus limits in the amount of resources available for research activities.

These are some of the reasons why sovereign ratings in particular give rise to many questions related to the independence and accountability of these institutions, private-owned and to some extent unregulated. The issue is even more delicate while considering the “regulatory abdication” in favor of CRAs[43] that seems to be in place in a number of countries, where some regulatory advantages directly stem from the ratings given (for instance, institutional investors may be subject to different obligations and regulatory burdens if investing in “investment grade” countries, compared to “speculative grade” ones).

Public institutions have recently realized that less reliance on credit rating agencies is desirable. For instance, the Financial Stability Board approved a document (“Principle for Reducing Reliance on CRA Ratings”) addressing the need to reduce the reliance expressed in standards, laws and regulations, as well as the reliance of the market (banks, firms, institutional investors), and of central banks[44].

After the financial turmoil, when CRAs were accused of poor performance, some regulatory answers came from the US (were the 2010 Dodd-Frank Act addressed the issue of the prevention of conflicts of interest, increasing internal controls for CRAs, requiring greater transparency, and providing SEC with stronger regulatory tools) and Europe (where European Reg. n. 1060/2009, amended by Reg. n. 513/2011 transferring responsibility to the European Securities and Markets Authority, provided a significant piece of industry-specific regulation). Key issues have been nevertheless largely left on the ground, and the European Parliament is planning to go back to the matter[45].

It is interesting to note that the sovereign rating activity expresses a significant link with time[46]. Nevertheless, if the concept of credit and time are directly linked (since credit is essentially a question about the future), the connection between ratings and time is somewhat more subtle and complex to grasp[47]. Therefore, it is not by chance that one of the major CRAs has addressed in a document the issue of the relationship between time and rating, according to which “for purposes of credit and credit ratings […] time absolutely exists and plays several key roles”[48]. Creditworthiness, as a result of the close connection of the concept of credit with that of time, will be subject to changes as the above conditions get modified. However, how these changes in sovereign ratings occur is not fully straightforward.

Credit ratings may be assigned in different ways, depending on the importance that is attached to elements of the business cycle, i.e. to elements that may be related to temporary conditions in the market. In relation to this, ratings may be alternatively “timely” (when concentrating on current views) or “forward-looking” (when substantially embodying analytic forecasts and projections). Generally speaking, ratings tend to be timely, i.e. at any point in time reflecting current views, even though partially corrected by the impact of relevant forecasts and projections. As a consequence, as soon as a change in the parameters above is verified for any sovereign, the rating is adjusted, in a way proportional to the magnitude of the change. The time lapsing between changes and modifications is solely due to the time needed to complete the analysis of new developments[49]. Only a minority advocates the need for a stability of ratings, against the so called “cliff effects”, i.e. sudden changes in credit ratings that deeply affect (or manipulate?) markets.

A further intersection between rating and time is represented by the time horizon of the ratings and the timing of rating changes. In striking a balance between being too fast and too slow in the adjustments, CRAs need to evaluate whether pieces of information represent the beginning of an emerging trend or rather random anomalies[50]. In order to do so, instruments like Credit Watch and Outlook are employed. While the former is used in case additional information is necessary to take a rating action, or when the magnitude of the rating impact has not been fully determined, the latter have a longer time horizon and incorporate trends or risks that have less-certain implications for credit quality[51].

The existence of multiple credit rating instruments related to time shows how delicate the relationship between time and sovereign power may be. In the slope in Figure 1, CRAs are represented as private subjects performing semi-public functions that imply a time acceleration greater than SWFs, but narrower than financial institutions. They have a lower degree of sovereign power than SWFs, since they do not directly perform activities that may affect sovereign prerogatives, but they cannot be considered as an ordinary player in the market, due to the influence that may be exerted upon decisions of sovereign States. The existence of instruments such as CreditWatch and Outlook further specifies the more or less intense time acceleration associated with credit rating.

In financial markets, time acceleration often takes the form of volatility. While CRAs argue that sovereign ratings are no more volatile than other credit ratings, the issue of volatility raises the question of the existence of alternatives to sovereign credit ratings. The market developed some instruments, that nevertheless present some problems, even worse than the those of sovereign ratings. The main alternative, in fact, is represented by Credit default swaps (“Cds”) over sovereign debt, i.e. insurances associated with the risk of default of the State emitting public debt titles. Once the market has been left alone in giving this evaluation, we may end up in having instruments even more reactive, with greater importance attached to sudden shifts in the trust towards sovereign States (thus ideally placing in a lower position in the slope under Figure 1)[52]. The advantage that Cds are able to quantify sovereign risks seems therefore to be exceeded by the fact that they carry incomplete information and are affected by a significant degree of opacity[53].

4. Tentative conclusions.

The article focused so far on issues that have been systematically addressed in the aftermath of the economic and financial crisis, like the relationship between finance and sovereign power, the rise of sovereign wealth funds, and the role of rating agencies. We argue, nevertheless, that the questions raised go well beyond factual contingencies, and force us to rethink partially the theoretical legal framework within which they are analyzed. In addition to this, many implications may follow in relation to a number of institutions and concepts of western legal tradition.

As a preliminary consideration, and from an epistemologic viewpoint, it is worth recalling that the knowledge at the basis of modern legal science that rests in public law upon the work of Hans Kelsen, owes much to Kant’s philosophy[54], which is in turn partially based upon Newtonian physics. The challenge imposed in science to classic physics, anyway, does not seem yet to have been taken fully into account within legal studies.

Anyway, there are authors now arguing that the theory of legal sources is being currently under challenge, as Newtonian physics has been in the past[55].

Even more interestingly, some authors explored the possibility of a curvature of the constitutional space following to the general theory of relativity, studying the impact that the law has in shaping the social background, that is too often taken as given[56]. In other words, the idea has been put forward that in case of collision between institutions, an alteration of the field of play takes place. Following to our analysis, it may be argued that both Sovereign Wealth Funds and Rating Agencies have altered the legal background in which they were created, being there no “neutral stage” on which actors can play from a legal point of view. In more general terms, the law (intended both as legal norm and legal concept) cannot extract itself neither from social structures[57], nor from economic ones.

The evolution verified in sciences following to “relativity revolution” seems to ultimately deny the possibility of isolation. The complex network of interaction between background and foreground, subject and object, observer and phenomena[58] represents a paradigm that seems to better fit the analysis of modern legal institutions. If SWFs are intrinsically able to shape the legal playing field in which they operate, CRAs behave much in the same way, being it verified that sovereign rating downgrades may well impact financial markets others than the one of the country[59].

As a consequence, the vocabulary and the taxonomy of public law in relation to sovereignty issues are to a certain extent lagging behind evolutions in the real world, and intuitions about them. Dissertations upon sovereignty often seem to keep as arrière-pensée the idea of a closed and independent system. Reality, anyway, seems to suggest the contrary, and specifically that sovereign entities are not unitary, coherent and independent systems any more. This idea may be easily proved going back to the foundations of contemporary economy, that is no longer an economy of imitation, but rather of innovation, for which valuable characteristics are communications and interdependence, rather than isolation and independence.

Having said that, the framework for the answer to the question whether a crisis of sovereignty is in place should be more clear. A valid help comes from the etymology of the word “crisis”, deriving from the ancient Greek verb κρίνειν (krìnein), literally “to separate”. No specific event or subject seems able to (have) put in crisis the notion of sovereignty by replacing it with a comparable one. Nevertheless, a change in the paradigms underlying sovereignty seems to be proved in the real world. Anyway, it is necessary to bear in mind that in science new phenomena may well emerge without reflecting destructively upon past scientific practice; a new theory does not necessary conflict with predecessors[60]. If the notion of sovereignty serves to explain part of the legal picture, there are elements that may be explained only by taking into consideration the temporal dimension.

Rather than a crisis of sovereignty, it seems to be more appropriate to talk about a “slow acceleration” of sovereign power, both in the evolution of the type of State (from Liberal State to Welfare State and to Market State) and in the functions (which we labeled as semi-public) performed by private entities. In this respect, sovereign power has come to be continuously under challenge, called to a permanent comparison with economic and political powers, on an equal footing with them.

Anyway, conceding that scientific paradigms have both a cognitive and a normative function, it becomes clear how a discussion upon the notion of sovereignty that puts into question from a cognitive viewpoint its ability to explain contemporary phenomena, may nevertheless maintain some normative meaning. From the analysis of the general relationship between sovereign power, time and finance, as well as from the enquiry over the main characteristics of Sovereign Wealth Funds and Rating Agencies, it seems appropriate to advocate in favor of an increase in accountability. For sovereign entities, because it is the main way to bring into light the overlaps with other powers; for SWFs, in order to extract possible advantages form them without put undue pressure upon sovereign States; and for CRAs, to let them perform their functions in the less invasive way possible.

Even more important, accountability would in this way serve as a counterweight to the danger of “market sovereignty”; that is no complement, but rather an alternative to liberal democracy[61].

Bibliography

Bassanini, Franco. The Law of Sovereign Wealth Funds. Introduction to The Law of Sovereign Wealth Funds, by Fabio Bassan, 1-10. London: Edward Elgar Publishing, 2011.

Bertoni, Fabio, Chiarlone, Stefano, Drezner, Daniel, Ferri, Giovanni and Goldstein, Andrea, “Fondi sovrani” Osservatorio monetario dell’Università Cattolica 3 (2008): 1-76.

Bin, Roberto. “Ordine delle norme e disordine dei concetti (e viceversa). Per una teoria quantistica delle fonti del diritto”. In Il diritto costituzionale come limite e regola al potere, edited by Giuditta Brunelli, Andrea Pugiotto and Paolo Veronesi, 35-60. Napoli: Jovene, 2009.

Bobbit, Philip. The Shield of Achilles: War, Peace and the Course of History. London: Allen Lane, 2002.

Bodin, Jean. Sei libri dello Stato. Torino: UTET, 1988.

Chirico, Alessandra. La sovranità monetaria tra ordine giuridico e processo economico. Padova: Cedam, 2003.

Cuocolo, Lorenzo. Tempo e potere nel diritto costituzionale. Milano: Giuffré, 2009.

European Central Bank. “The Accumulation of Foreign Reserves” Occasional Paper 43 (2006): 7-25.

Enriques, Luca, and Gargantini, Matteo. “Regolamentazione dei mercati finanziari, rating e regolamentazione del rating.” Analisi Giuridica dell’Economia 2 (2010): 475-502.

Financial Stability Board, Principles for Reducing Reliance on CRA Ratings, 27 October 2010, http://www.financialstabilityboard.org /publications/r_101027.pdf.

Gieve, John. “Sovereign Wealth Funds and Global Imbalances”. Bank of England Quarterly Bulletin 2 (2008): 196-202.

Habermas, Jürgen. La costellazione post-nazionale. Milano: Feltrinelli, 1999.

Hobsbawm, Eric J.. La fine dello Stato. Milano: Rizzoli, 2007.

Holmes, Stephen, and Sunstein Cass R.. The Cost of Rights. Why Liberty Depends on Taxes. London-New York: W.W. Norton and Company, 1999.

International Monetary Fund. Sovereigns, Funding and Systemic Liquidity (Global Financial Stability Report: 2010), 1-122.

Kindleberger Charles P.. A Financial History of Western Europe. Oxford-New York: Oxford University Press, 1993.

Kuhn, Thomas S.. The Structure of Scientific Revolutions. Chicago: The University of Chicago Press, 1962.

Luttwak, Edward N.. Turbo-Capitalism. Winners and Losers in the Global Economy. New York: Harper Collins, 1999.

Lyons, Gerard. “State Capitalism: The Rise of Sovereign Wealth Funds” Journal of Management Research 3 (2007): 119-146.

Macchiati, Alfredo. “L’interesse pubblico nella regolamentazione finanziaria.” Mercato, concorrenza, regole, 2 (2009): 223-248.

MacCormick, Neil. Questioning Sovereignty. Oxford: Oxford University Press, 1999.

Mezzacapo, Simone. “The So-Called Sovereign Wealth Funds: Regulatory Issues, Financial Stability and Prudential Supervision.” European Commission, Economic and Financial Affairs DG, Economic Paper 378 (2009): 42-62.

Napolitano, Giulio. “Il nuovo Stato salvatore: strumenti di intervento e assetti istituzionali.” Giornale di diritto amministrativo 11 (2008): 1083-1094.

O’Connor, James R.. The Fiscal Crisis of the State. New York: St. Martin’s Press, 1973.

Ost, François, and van de Kerchove, Michel. De la pyramide au résau? Pour une théorie dialectique du droit. Bruxelles: Publications des Facultés universitaires Saint-Louis, 2002.

Padoa-Schioppa, Tommaso. La veduta corta. Bologna: Il Mulino, 2009.

Paulson, Stanley “The Neo-Kantian Dimension of Kelsen’s Legal Theory” Oxford Journal of Legal Studies 12 (1992): 311-332.

Richardson, Matthew and White, Lawrence J. White, “The Rating Agencies. Is Regulation the Answer?”, in Restoring Financial Stability. How to Repair a Failed System, edited by Viral V. Acharya and Matthew Richardson. Hoboke: Wiley, 2009.

Rifkin, Jeremy. The Age of Access: How the Shift from Ownership to Access is Transforming Modern Life. London: Penguin Books, 2000.

Rossi, Guido. Foreword to Posner, Richard A., La crisi della democrazia capitalista. Milano: Università Bocconi Editore, 2010.

Schmitt, Carl. Die Lage der europaïschen Rechtswissenschaft. Tübingen: Universität-Verlag, 1950.

Schmitt, Carl. Der Nomos der Erde im Völkerrecht des Jus Publicum Europaeum. Berlin: Duncker&Humblot, 1950.

Slaughter, Anne-Marie. A New World Order. Princeton: Princeton University Press, 2004.

Standard and Poor’s, Sovereign Credit Ratings: A Primer, 29 May 2008, [http://www.standardandpoors.com/prot/ratings/articles/en/eu/? article->http://www.standardandpoors.com/prot/ratings/articles/en/eu/?%20article]Type=HTML&assetID=1245319266873.

Standard and Poor’s, The Time Dimension Of Standard & Poor’s Credit Ratings, 22 September 2010, [http://www.standardandpoors.com/ about-sp/articles/en/us/?article->http://www.standardandpoors.com/%20about-sp/articles/en/us/?article]Type=HTML&assetID=1245226256386.

Standard and Poor’s, The Wishes of Crowds: Do Credit Spreads Measure Credit Risk?, 13 December 2010, [http://www.standardandpoors.com/prot/ratings/->http://www.standardandpoors.com/prot/ratings/]articles/en/eu/?articleType=HTML&assetID=1245271294101

Standard and Poor’s, Sovereign Defaults And Rating Transition Data. Update 2010, 23 February 2011, http://www.standardandpoors. com/prot/ratings/articles/en/eu/?articleType=HTML&assetID=1245300338976.

Standard and Poor’s, Sovereigns: Sovereign Government Rating Methodology And Assumptions, 30 June 2011, http://www. standardandpoors.com/prot/ratings/articles/en/eu/?assetID=1245315323295.

Stigler, George J.. “The Theory of Economic Regulation.” The Bell Journal of Economics and Management Science, 1 (1971): 3-21.

Summers, Lawrence H.. “Sovereign funds shake the logic of capitalism.” Financial Times, July 30, 2007.

Tribe, Laurence H.. “The Curvature Of Constitutional Space: What Lawyers Can Learn From Modern Physics.” Harvard Law Review, 1 (1989): 1-39.

[1] Paragraphs 1 and 4 belong to Lorenzo Cuocolo, whereas paragraphs 2 and 3 belong to Valentina Miscia. A draft version of the article was presented to the W.G. Hart Legal Workshop “Sovereignty in Question” organized by the Institute of Advanced Legal Studies in London on 28-30 June 2011. Lorenzo Cuocolo is Professor of Comparative Public Law at Bocconi University in Milan. Valentina Miscia is LLM candidate at the London School of Economics and Political Science (2012) and Ph.D. candidate in International Law and Economics and Bocconi University (2014).

[2] Charles P. Kindleberger, A Financial History of Western Europe (Oxford-New York: Oxford University Press, 1993), 42-43.

[3] Lorenzo Cuocolo, Tempo e potere nel diritto costituzionale (Milano: Giuffré, 2009), 6 ff.

[4] Cuocolo, Tempo e potere, 93 ff.

[5] Carl Schmitt, Die Lage der europaïschen Rechtswissenschaft (Tübingen: Universität-Verlag, 1950), passim.

[6] Carl Schmitt, The Nomos oft he Earth in the International Law of the Jus Publicum Europeum (New York: Telos, 2003), 351 ff.

[7] Jürgen Habermas, The Postnational Constellation. Political Essays (Cambridge: MIT Press, 2001),

[8] Stephen Holmes and Cass R. Sunstein, The Cost of Rights. Why Liberty Depends on Taxes (London-New York: W.W. Norton and Company, 1999), 58 ff.

[9] James R. O’Connor, The Fiscal Crisis of the State (New York: St. Martin’s Press, 1973), passim.

[10] An idea of “Market State” is discussed in Philip Bobbit, The Shield of Achilles: War, Peace and the Course of History (London: Allen Lane, 2002).

[11] Giulio Napolitano, “Il nuovo Stato salvatore: strumenti di intervento e assetti istituzionali”, Giornale di diritto amministrativo, 11 (2008): 6-7.

[12] François Ost and Michel van de Kerchove, De la pyramide au résau? Pour une théorie dialectique du droit (Bruxelles: Publications des Facultés universitaires Saint-Louis, 2002), 11-22, 79-88, 143-158.

[13] Anne-Marie Slaughter, A New World Order (Princeton: Princeton University Press, 2004), 12 ff.

[14] George J. Stigler, “The Theory of Economic Regulation”, The Bell Journal of Economics and Management Science 1 (1971): 3-21.

[15] Alfredo Macchiati, “L’interesse pubblico nella regolamentazione finanziaria”, Mercato, concorrenza, regole 2 (2009): 223-248.

[16] Much debate has arisen around the idea of imposing such limits in constitutional texts, following the German example (see articles 109 and 115 Grundgesetz).

[17] Cuocolo, Tempo e potere, 271 ff.

[18] Edward N. Luttwak, Turbo-Capitalism. Winners and Losers in the Global Economy (New York: Harper Collins, 1999), passim.

[19] After the original order has been put into the system, financial institutions running the HFT enjoy a thirty-millisecond time through which they are enabled to get the preview of the order, analyze it, and put other orders into the system following to the analysis, before the original order hits the marketplace.

[20] This is the acronym for the Markets in Financial Instruments Directive, whose revision is due in the forthcoming months (proposal of the European Commission for a Directive on markets in financial instruments repealing Directive 2004/39/EC of the European Parliament and of the Council, presented on 20 October 2011).

[21] European Central Bank, “The Accumulation of Foreign Reserves” Occasional Paper 43 (2006): 7-25.

[22] John Gieve, “Sovereign Wealth Funds and Global Imbalances” Bank of England Quarterly Bulletin 2 (2008): 196-202. See also Fabio Bertoni et al., “Fondi sovrani” Osservatorio monetario dell’Università Cattolica 3 (2008): 1-76.

[23] Franco Bassanini, The Law of Sovereign Wealth Funds, foreword to Fabio Bassan, The Law of Sovereign Wealth Funds (Cheltenham: Edward Elgar, 2011), viii-xvi.

[24] Guido Rossi, Foreword to Richard A. Posner, La crisi della democrazia capitalista, (Milano: Università Bocconi Editore, 2010), vii-xviii.

[25] Bassanini, The Law of Sovereign Wealth Funds, viii-xvi.

[26] Lawrence H. Summers, “Sovereign funds shake the logic of capitalism”, Financial Times, July 30, 2007.

[27] Gerard Lyons, “State Capitalism: The Rise of Sovereign Wealth Funds”, Journal of Management Research 3 (2007): 119-146.

[28] Guido Rossi, Foreword, xii-xviii.

[29] Simone Mezzacapo, “The So-Called Sovereign Wealth Funds: Regulatory Issues, Financial Stability and Prudential Supervision”, European Commission, Economic and Financial Affairs DG, Economic Paper 378 (2009): 42-62.

[30] Neil MacCormick, Questioning Sovereignty (Oxford: Oxford University Press, 1999), 127.

[31] Jeremy Rifkin, The Age of Access: How the Shift from Ownership to Access is Transforming Modern Life (London: Penguin Books, 2000), passim.

[32] Jean Bodin, Sei libri dello Stato (Torino: UTET, 1988), 495.

[33] Alessandra Chirico, La sovranità monetaria tra ordine giuridico e processo economico (Padova: Cedam, 2003), 18, 72.

[34] Tommaso Padoa-Schioppa, La veduta corta (Bologna: Il Mulino, 2009), passim.

[35] Bassanini, The Law of Sovereign Wealth Funds, viii-xvi.

[36] Luca Enriques and Matteo Gargantini, “Regolamentazione dei mercati finanziari, rating e regolamentazione del rating” Analisi Giuridica dell’Economia 2 (2010): 475-502.

[37] International Monetary Fund, Sovereigns, Funding and Systemic Liquidity (Global Financial Stability Report: 2010), 88-118.

[38] International Monetary Fund, Sovereigns, Funding and Systemic Liquidity, 88-97.

[39] Taking as an example Standard and Poor’s methodology. Even with slight differences, the conclusions drawn would hold much in the same way for other CRAs.

[40] Standard and Poor’s, Sovereigns: Sovereign Government Rating Methodology And Assumptions, 30 June 2011, [http://www.standardandpoors.com/prot/ratings/articles/en->http://www.standardandpoors.com/prot/ratings/articles/en] /eu/?assetID=1245315323295.

[41] In a previous version of the document the parameters were articulated as follows: a) political risk: institutions (stability, predictability, transparency), systems, processes (independent judiciary, civil society, free press, adversary politics, changes in government, public security, relations with neighboring countries); b) economic structure and economic growth prospects: legal enforceability of property rights, per-capita GDP, development of the financial system, degree of income equality, development of the private sector, efficiency of the public sector; c) fiscal flexibility: government revenue and expenditure (flexibility, effectiveness, appropriateness), balance performance, fiscal stance, debt and interest burden characteristics and trends, off-budget and contingent liabilities, pension obligations; d) off-budget and contingent liabilities: presence and profitability of non-financial public sector enterprises, financial sector (possible liquidity and solvency problems); e) monetary flexibility: monetary policy (appropriateness, effectiveness and market orientation), depth of financial sector and capital markets; f) external liquidity and external debt burden: ability to generate foreign exchange, gross external financing needs, external balance sheet. Standard and Poor’s, Sovereign Credit Ratings: A Primer, 29 May 2008, [http://www.standardandpoors.com/prot/ratings/articles/en/eu/?article->http://www.standardandpoors.com/prot/ratings/articles/en/eu/?article]Type=HTML&assetID=1245319266873.

[42] Standard and Poor’s, Sovereign Defaults And Rating Transition Data. Update 2010, 23 February 2011, [http://www.standardandpoors.com/prot/ratings/articles/en/eu/->http://www.standardandpoors.com/prot/ratings/articles/en/eu/]? articleType=HTML&assetID=1245300338976.

[43] Enriques and Gargantini, Regolamentazione dei mercati finanziari, 475-502.

[44] Financial Stability Board, Principles for Reducing Reliance on CRA Ratings, 27 October 2010, http://www.financialstabilityboard.....

[45] See the discussion of the plenary session of 6th June 2011 over the “Report on rating agencies: future perspectives” adopted by the EP Committee on Economic and Monetary Affairs, were the possibility of further reviewing the legislation in place is examined, along with the creation of a European Credit Rating Foundation

[46] The importance of the timing aspect of rating is well recognized; among others, Matthew Richardson and Lawrence J. White, “The Rating Agencies. Is Regulation the Answer?”, in Restoring Financial Stability. How to Repair a Failed System, ed. Viral V. Acharya et al. (Hoboke: Wiley, 2009), 111-112.

[47] Standard and Poor’s, The Time Dimension Of Standard & Poor’s Credit Ratings, 22 September 2010, [http://www.standardandpoors.com/about-sp/articles/en/us/?article->http://www.standardandpoors.com/about-sp/articles/en/us/?article] Type=HTML&assetID=1245226256386.

[48] Standard and Poor’s, The Time Dimension.

[49] Standard and Poor’s, The Time Dimension.

[50] Standard and Poor’s, The Time Dimension.

[51] Standard and Poor’s, The Time Dimension.

[52] Enriques and Gargantini, Regolamentazione dei mercati finanziari, 475-502.

[53] Standard and Poor’s, The Wishes of Crowds: Do Credit Spreads Measure Credit Risk?, 13 December 2010, [http://www.standardandpoors.com/prot/ratings/->http://www.standardandpoors.com/prot/ratings/] articles/en/eu/?articleType=HTML&assetID=1245271294101.

[54] Stanley Paulson, “The Neo-Kantian Dimension of Kelsen’s Legal Theory” Oxford Journal of Legal Studies 12 (1992): 325-326.

[55] Roberto Bin, “Ordine delle norme e disordine dei concetti (e viceversa). Per una teoria quantistica delle fonti del diritto”, in Il diritto costituzionale come limite e regola al potere, ed. Giuditta Brunelli et al. (Napoli: Jovene, 2009), 35-60.

[56] Laurence H. Tribe, “The Curvature Of Constitutional Space: What Lawyers Can Learn From Modern Physics” Harvard Law Review 1 (1989), 1-39.

[57] Tribe, The Curvature Of Constitutional Space, 7.

[58] Tribe, The Curvature Of Constitutional Space, 25-39.

[59] International Monetary Fund, Sovereigns, Funding and Systemic Liquidity, 88-117.

[60] Thomas S. Kuhn, The Structure of Scientific Revolutions (Chicago: The University of Chicago Press, 1962), passim.

[61] Eric J. Hobsbawm La fine dello Stato (Milano: Rizzoli, 2007), passim.

your comment